Why C&I Solar Projects in Europe Are Adding BESS (Germany Case Study)

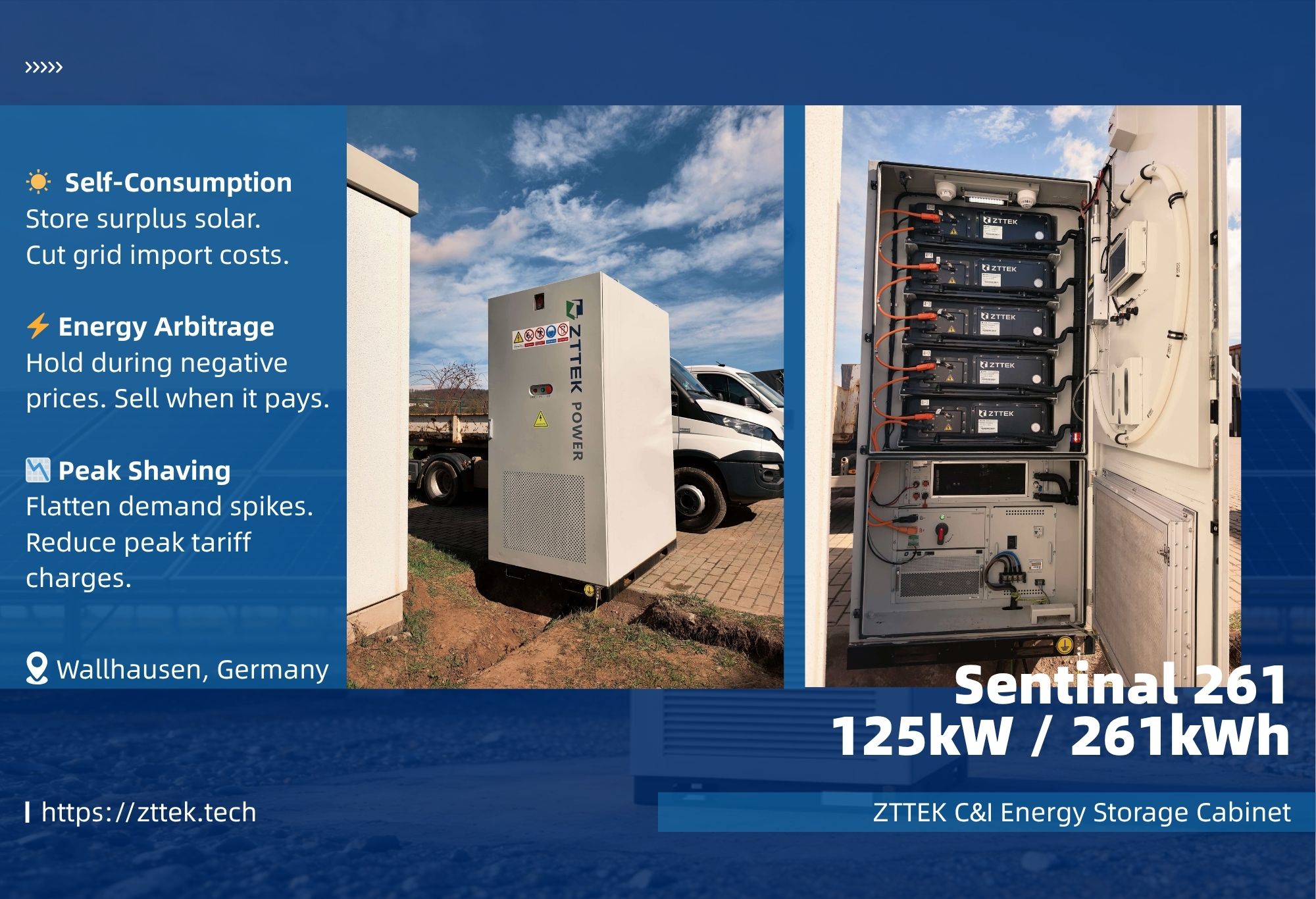

A farm in Wallhausen, Germany recently brought a ZTTEK Sentinal 261 commercial battery energy storage system alongside its 450 kW PV installation. The use case is straightforward: capture surplus solar generation, avoid exporting during negative price hours, and reduce electricity costs over the long term.

The project is live. The system is running. And the challenge it solves is not uniquely German.

Negative Electricity Prices Are Now a Pan-European Problem

When people think of negative electricity prices in Europe, they tend to think of Germany. But the picture in 2024 and 2025 tells a different story.

Spain recorded no negative price hours as recently as 2023, yet within a single year that figure jumped to nearly 770 hours. By September 2025, Spain had already logged over 500 negative-price hours for the year — more than double its full-year 2024 total. Poland, Greece, the Netherlands, and Romania have all seen sharp increases. Across Europe as a whole, 2024 saw nearly 4,838 zero or negative price hours — close to double the year before.

The driver is the same everywhere: solar and wind capacity is expanding faster than grids can absorb it. As one energy analyst put it, negative prices will not disappear — the growth of solar and wind will keep pushing price volatility higher, and only a significant scaling up of storage can reduce it.

For C&I solar operators and EPC developers across Southern and Eastern Europe, this trend is increasingly hard to ignore. Markets that had little or no negative pricing exposure two years ago now face regular mid-day price suppression during peak solar hours — exactly when their assets are generating the most power.

What the Wallhausen Project Demonstrates

The farm in Wallhausen operates a 450 kW solar installation — significant generation capacity for a single agricultural site. Without storage, a substantial share of its midday output would be exported to the grid at whatever spot price prevailed in that moment. As the data above shows, that price is increasingly likely to be very low, or negative.

The Sentinal 261 BESS addresses this in two ways:

Self-consumption first. The battery absorbs surplus PV output during peak generation periods and holds it for use during the evening, when grid import costs are higher. This directly lowers the farm’s electricity bill without touching the grid.

Export timing control. When spot prices go negative, the system holds generation rather than forcing export. Discharge is scheduled for periods when the price is positive — converting what would have been a loss into a usable revenue or cost-avoidance event.

This combination — self-consumption optimization plus negative-price avoidance — is a financially compelling pairing for any solar site operating under European market conditions today. The economics look particularly strong in markets where negative pricing is still relatively new and storage adoption is low, meaning grid volatility is high and competition for arbitrage windows is limited.

Why Less-Established Markets May Offer the Better Opportunity

Germany’s commercial battery storage market is maturing quickly. Installer competition is high, margins are compressed, and grid policy is well-developed. For EPC developers and C&I energy buyers evaluating where to focus next, markets like Spain, Italy, Poland, and Romania present a different set of conditions.

Spain and Portugal are now leading Europe in negative-price frequency, and the pattern is concentrated in spring and early summer — precisely when solar generation peaks. Italy has so far avoided negative prices through market regulation, but has seen a steady increase in ultra-low price hours, and policy changes are already underway in response. In Eastern Europe, Romania and Hungary recorded the highest price volatility in Europe in 2024 — a market condition that makes dispatchable storage assets disproportionately valuable.

In each of these markets, commercial battery storage adoption is earlier-stage than in Germany. Grid infrastructure is often less flexible, making price swings more severe and storage more impactful when it is deployed. And project pipelines are growing rapidly as solar capacity expands.

For installers and EPCs looking to build out a BESS project portfolio in Europe, this is the window before the market gets crowded.

The System: ZTTEK Sentinal 261

The system deployed at Wallhausen is the Sentinal 261, part of ZTTEK’s C&I BESS cabinet series. Key specifications:

-

Energy capacity: 261 kWh (314 Ah LFP, 1P52S, 832 V nominal)

-

Rated AC power: 125 kW (peak: 137 kW)

-

Cooling: Liquid cooling for stable long-term thermal management

-

Operating temperature: -20°C to 50°C

-

Fire protection: Multi-level, cluster and pack level (perfluorohexanone or aerosol)

-

Communication: RS485 / CAN; third-party EMS compatible

-

Protection: IP54 for outdoor and semi-outdoor deployment

-

Certifications: IEC 62619, IEC 63056, CE-EMC, CE-LVD, UN38.3

The liquid-cooled architecture is well-suited to the variable climates of Southern and Eastern Europe — maintaining consistent thermal conditions across the charge/discharge cycles that arbitrage and self-consumption strategies require year-round. IP54 enclosure and a wide operating temperature range mean the system can be deployed outdoors across a broad range of site configurations.

The Wallhausen installation marks ZTTEK’s first operational C&I BESS deployment in the European market. The system is field-validated and grid-certified for deployment across EU markets.

For EPC Developers and C&I Buyers

If you’re evaluating commercial battery storage for a solar project in Europe — whether that’s an agricultural site in Spain, a light industrial facility in Poland, or a commercial building in Italy — the economics underpinning the Wallhausen project apply directly.

Solar assets without storage are increasingly price-exposed. Battery energy storage systems turn that exposure into a manageable, and potentially profitable, operating condition. The markets where this matters most right now are not the ones that have already built out their storage infrastructure — they’re the ones where the solar is growing fast and the batteries haven’t caught up yet.