The C&I Solar + BESS Playbook for European Project Developers

A practical guide to commercial battery storage for C&I solar projects in Europe — covering business case fundamentals, system design, integration, and which markets offer the best opportunity in 2025 and beyond.

Something shifted in the European C&I energy market in the last two years, and it wasn't subtle.

Solar is cheaper than ever. Grid electricity is volatile. Energy costs are a boardroom issue at manufacturers, logistics operators, farms, and commercial property owners across the continent. And for the first time, the business case for pairing battery storage with commercial solar is consistently closing — without subsidies, without complexity, and without a decade-long payback period.

European C&I BESS is projected to grow at a 71% CAGR through 2028, and the sector is expected to see over 60% growth in installations in 2025 alone. Those are not residential numbers driven by government incentive schemes. They reflect real project economics — businesses doing the math and finding that storage pays.

This guide is for EPC developers, system integrators, and C&I energy buyers who want to understand how commercial battery storage actually works in a European project context: the business case, the system design considerations, the integration requirements, and where the opportunity is most interesting right now.

Solar is cheaper than ever. Grid electricity is volatile. Energy costs are a boardroom issue at manufacturers, logistics operators, farms, and commercial property owners across the continent. And for the first time, the business case for pairing battery storage with commercial solar is consistently closing — without subsidies, without complexity, and without a decade-long payback period.

European C&I BESS is projected to grow at a 71% CAGR through 2028, and the sector is expected to see over 60% growth in installations in 2025 alone. Those are not residential numbers driven by government incentive schemes. They reflect real project economics — businesses doing the math and finding that storage pays.

This guide is for EPC developers, system integrators, and C&I energy buyers who want to understand how commercial battery storage actually works in a European project context: the business case, the system design considerations, the integration requirements, and where the opportunity is most interesting right now.

Why the Business Case Has Finally Matured

For most of the last decade, the C&I BESS conversation in Europe went in circles. The hardware was expensive. The revenue streams were thin. The grid integration was complicated. And most C&I operators didn't have an energy team sophisticated enough to manage a storage asset.

Three things changed.

LFP cell costs fell off a cliff. Lithium iron phosphate packs are now approaching USD 100 per kWh — a threshold that makes C&I battery storage financially viable across a wide range of site profiles without needing to stack every possible revenue stream to justify the investment.

Energy price volatility became structural, not temporary. The 2021–2022 energy crisis was a shock. What followed it wasn't a return to stability — it was a European grid that is now permanently more volatile as fossil generation retires and renewables scale up. Grid curtailment cost German consumers alone €3 billion in a single year, and the pattern is repeating across Southern and Eastern Europe. For C&I operators with solar assets, this volatility is a risk without storage and an opportunity with it.

The regulatory environment is moving in the right direction. The EU's push on demand flexibility, smart metering, and energy communities is creating new revenue pathways for behind-the-meter storage assets. In more advanced markets, enrolling C&I BESS in demand response programs or virtual power plants further improves the business case — and those market structures are expanding to countries that didn't have them two years ago.

The result: BESS can reduce C&I energy costs by up to 80% when applied across peak shaving, self-consumption optimization, and renewable integration — a figure that was theoretical five years ago and is becoming routine in well-designed projects today.

Three things changed.

LFP cell costs fell off a cliff. Lithium iron phosphate packs are now approaching USD 100 per kWh — a threshold that makes C&I battery storage financially viable across a wide range of site profiles without needing to stack every possible revenue stream to justify the investment.

Energy price volatility became structural, not temporary. The 2021–2022 energy crisis was a shock. What followed it wasn't a return to stability — it was a European grid that is now permanently more volatile as fossil generation retires and renewables scale up. Grid curtailment cost German consumers alone €3 billion in a single year, and the pattern is repeating across Southern and Eastern Europe. For C&I operators with solar assets, this volatility is a risk without storage and an opportunity with it.

The regulatory environment is moving in the right direction. The EU's push on demand flexibility, smart metering, and energy communities is creating new revenue pathways for behind-the-meter storage assets. In more advanced markets, enrolling C&I BESS in demand response programs or virtual power plants further improves the business case — and those market structures are expanding to countries that didn't have them two years ago.

The result: BESS can reduce C&I energy costs by up to 80% when applied across peak shaving, self-consumption optimization, and renewable integration — a figure that was theoretical five years ago and is becoming routine in well-designed projects today.

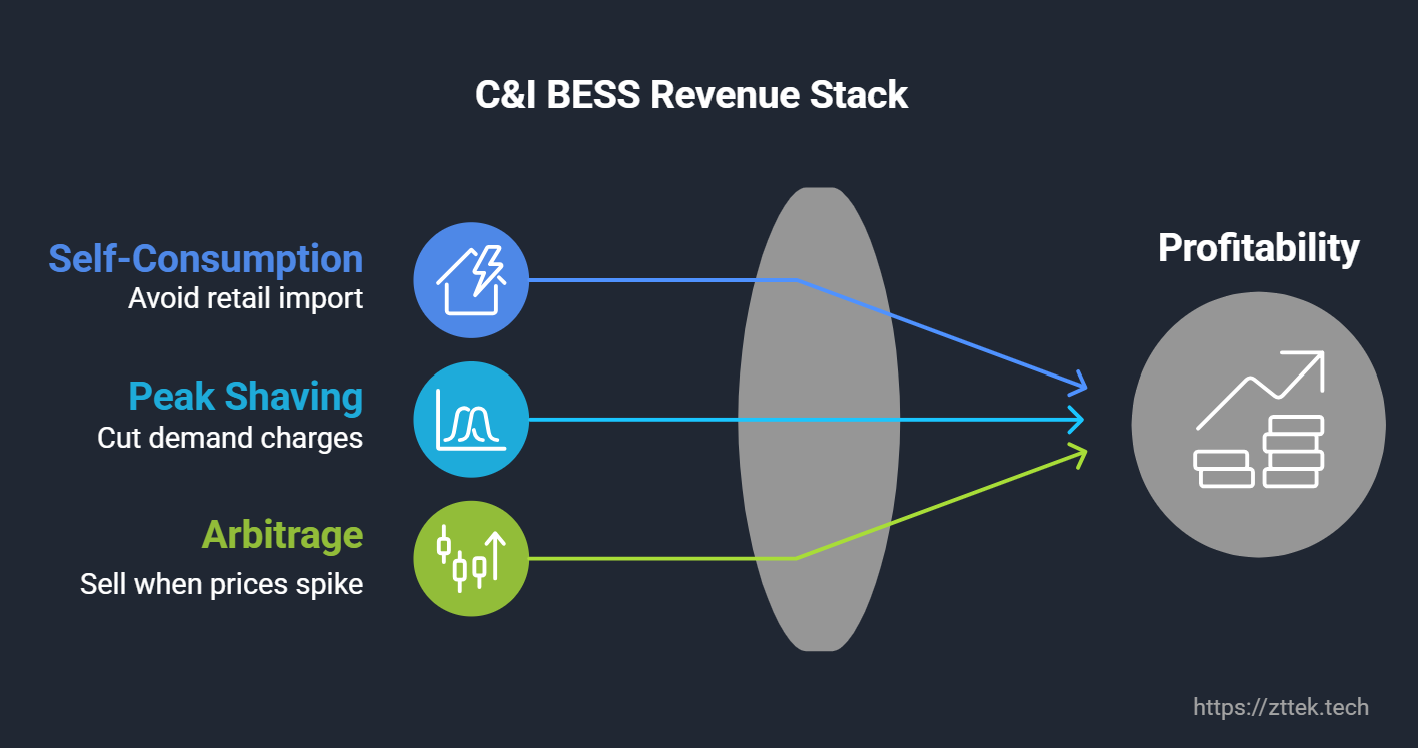

The Three Revenue Levers (and How They Stack)

The most important thing to understand about C&I BESS economics is that single-use-case projects rarely have the strongest returns. The best projects stack multiple value streams from the same asset, using the same hardware and a flexible control layer to dispatch energy intelligently across different market conditions.

1. PV Self-Consumption Optimization

This is the baseline use case, and it works everywhere solar is deployed. Without storage, surplus PV generation that exceeds site demand gets exported to the grid — often at compressed midday prices, increasingly at negative ones. A BESS captures that surplus and holds it for site use in the evening, effectively replacing grid import at retail tariff rates.

The economics are straightforward: the spread between your avoided grid import price and your solar marginal cost is your return. In countries with high retail tariffs — Spain, Italy, Germany, Poland — this spread is substantial and growing.

2. Peak Shaving and Demand Charge Reduction

Many C&I electricity tariffs include a demand charge component — a fee based on peak consumption during a billing period, often the highest 15–30 minute window of the month. A BESS dispatched at peak moments can flatten that spike, reducing the demand charge significantly without affecting operations.

This use case is particularly valuable for manufacturing facilities, cold storage operators, logistics hubs, and any site with predictable high-draw loads. The return is deterministic — it shows up on every bill — which makes it the most bankable component of a C&I BESS business case.

3. Energy Arbitrage and Negative-Price Management

As we covered in our case study from Wallhausen, Germany, the ability to time grid export and import is increasingly valuable in European electricity markets. Spain is expected to climb into the top 5 European battery markets in 2025, in large part because its solar penetration has reached a level where mid-day price suppression is regular and severe. Italy, Poland, and Romania are following similar trajectories.

A BESS that can hold generation during low or negative price periods and discharge when prices recover turns a price-exposed solar asset into a dispatchable one. This is the use case that will define C&I storage economics in Southern and Eastern Europe over the next five years.

1. PV Self-Consumption Optimization

This is the baseline use case, and it works everywhere solar is deployed. Without storage, surplus PV generation that exceeds site demand gets exported to the grid — often at compressed midday prices, increasingly at negative ones. A BESS captures that surplus and holds it for site use in the evening, effectively replacing grid import at retail tariff rates.

The economics are straightforward: the spread between your avoided grid import price and your solar marginal cost is your return. In countries with high retail tariffs — Spain, Italy, Germany, Poland — this spread is substantial and growing.

2. Peak Shaving and Demand Charge Reduction

Many C&I electricity tariffs include a demand charge component — a fee based on peak consumption during a billing period, often the highest 15–30 minute window of the month. A BESS dispatched at peak moments can flatten that spike, reducing the demand charge significantly without affecting operations.

This use case is particularly valuable for manufacturing facilities, cold storage operators, logistics hubs, and any site with predictable high-draw loads. The return is deterministic — it shows up on every bill — which makes it the most bankable component of a C&I BESS business case.

3. Energy Arbitrage and Negative-Price Management

As we covered in our case study from Wallhausen, Germany, the ability to time grid export and import is increasingly valuable in European electricity markets. Spain is expected to climb into the top 5 European battery markets in 2025, in large part because its solar penetration has reached a level where mid-day price suppression is regular and severe. Italy, Poland, and Romania are following similar trajectories.

A BESS that can hold generation during low or negative price periods and discharge when prices recover turns a price-exposed solar asset into a dispatchable one. This is the use case that will define C&I storage economics in Southern and Eastern Europe over the next five years.

System Design: What Actually Matters

A lot of C&I BESS procurement conversations get stuck on kWh price. That's understandable — hardware cost is visible and comparable. But the decisions that determine whether a project delivers its projected returns over a 10–15 year lifetime are rarely about the unit cost of storage.

Thermal management. Cycle life and long-term performance are directly linked to how well the system manages cell temperature. Liquid-cooled architectures maintain tighter temperature control across the operating range compared to air-cooled systems — a meaningful advantage for systems that are cycling daily, operating in high-ambient environments like Southern Europe, or deployed in locations with significant seasonal temperature variation. The additional upfront cost of liquid cooling is typically recovered through reduced degradation and longer useful life.

Power rating vs. energy capacity. These two parameters define what a BESS can actually do in a project. A system with high energy capacity but limited power output can't flatten a sharp demand spike. A high-power system with limited energy can't cover a multi-hour backup window. For most C&I projects, the ratio of power to energy should be matched to the dominant use case — usually 0.5C (half the energy capacity in rated power) for arbitrage and self-consumption applications.

Cabinet vs. all-in-one architecture. Larger C&I sites — farms, factories, logistics facilities — typically benefit from cabinet-based BESS that can be expanded incrementally. Cabinet systems allow phased investment, support multi-cabinet parallel operation, and can be scaled as site load grows or additional PV is added. All-in-one systems are better suited to space-constrained installations or projects where a single self-contained unit covers the full requirement.

Depth of discharge. The usable energy in a BESS is determined by its DoD — the percentage of rated capacity that can be used without accelerating degradation. Systems rated at 98% DoD deliver meaningfully more usable energy from the same installed capacity compared to those operating at 80–90%.

Thermal management. Cycle life and long-term performance are directly linked to how well the system manages cell temperature. Liquid-cooled architectures maintain tighter temperature control across the operating range compared to air-cooled systems — a meaningful advantage for systems that are cycling daily, operating in high-ambient environments like Southern Europe, or deployed in locations with significant seasonal temperature variation. The additional upfront cost of liquid cooling is typically recovered through reduced degradation and longer useful life.

Power rating vs. energy capacity. These two parameters define what a BESS can actually do in a project. A system with high energy capacity but limited power output can't flatten a sharp demand spike. A high-power system with limited energy can't cover a multi-hour backup window. For most C&I projects, the ratio of power to energy should be matched to the dominant use case — usually 0.5C (half the energy capacity in rated power) for arbitrage and self-consumption applications.

Cabinet vs. all-in-one architecture. Larger C&I sites — farms, factories, logistics facilities — typically benefit from cabinet-based BESS that can be expanded incrementally. Cabinet systems allow phased investment, support multi-cabinet parallel operation, and can be scaled as site load grows or additional PV is added. All-in-one systems are better suited to space-constrained installations or projects where a single self-contained unit covers the full requirement.

Depth of discharge. The usable energy in a BESS is determined by its DoD — the percentage of rated capacity that can be used without accelerating degradation. Systems rated at 98% DoD deliver meaningfully more usable energy from the same installed capacity compared to those operating at 80–90%.

Integration: The Part Most Projects Get Wrong

Hardware selection matters. Integration is where C&I BESS projects most commonly underdeliver.

A battery cabinet sitting on a site doesn't do anything useful without a control layer that knows when to charge, when to discharge, and at what rate. The sophistication of that control layer — and its ability to connect to the broader energy systems on site — is what separates a BESS that recovers its cost from one that sits at 50% utilization for most of its life.

There are two integration approaches worth understanding.

Standalone EMS operation. Most commercial BESS include a built-in Energy Management System that can execute basic scheduling strategies — charge from solar, discharge at peak, hold during negative price hours. For sites without existing building automation or third-party energy management platforms, this is the starting point. It's sufficient for most self-consumption and peak shaving use cases.

Open API integration. This is where things get more interesting. A BESS with local communication interfaces (RS485, CAN) and cloud API access can be connected to a building management system, a third-party EMS, a VPP aggregator, or a demand flexibility platform. This opens access to revenue streams that a standalone BESS simply cannot participate in — demand response programs, grid balancing services, energy community dispatch, and advanced time-of-use optimization.

For EPC developers designing systems that need to evolve as their clients' energy strategies mature, open integration capability is not optional. It's the difference between a BESS that remains useful for 15 years and one that becomes obsolete when the market structure changes.

A battery cabinet sitting on a site doesn't do anything useful without a control layer that knows when to charge, when to discharge, and at what rate. The sophistication of that control layer — and its ability to connect to the broader energy systems on site — is what separates a BESS that recovers its cost from one that sits at 50% utilization for most of its life.

There are two integration approaches worth understanding.

Standalone EMS operation. Most commercial BESS include a built-in Energy Management System that can execute basic scheduling strategies — charge from solar, discharge at peak, hold during negative price hours. For sites without existing building automation or third-party energy management platforms, this is the starting point. It's sufficient for most self-consumption and peak shaving use cases.

Open API integration. This is where things get more interesting. A BESS with local communication interfaces (RS485, CAN) and cloud API access can be connected to a building management system, a third-party EMS, a VPP aggregator, or a demand flexibility platform. This opens access to revenue streams that a standalone BESS simply cannot participate in — demand response programs, grid balancing services, energy community dispatch, and advanced time-of-use optimization.

For EPC developers designing systems that need to evolve as their clients' energy strategies mature, open integration capability is not optional. It's the difference between a BESS that remains useful for 15 years and one that becomes obsolete when the market structure changes.

Where to Focus: The European Markets Worth Watching

Germany currently accounts for around 30% of European BESS revenue, but grid connection queues are stretching to 18 months or longer, and the market is maturing rapidly. For EPC developers and distributors looking to build a project portfolio with meaningful upside, the more interesting opportunity is in markets where storage adoption is earlier-stage and the conditions that make storage valuable — solar penetration, price volatility, retail tariff levels — are already present.

Spain has transformed from minimal storage activity to one of the fastest-growing markets in Europe in 24 months, driven by solar penetration that now regularly produces midday price suppression. Spain had the fifth largest battery storage fleet in Europe by end of 2024, with utility-scale revival expected to drive further growth in 2025.

Italy combines high retail electricity prices, strong solar irradiance, a mature PV installation base, and progressive energy community legislation. Battery attachment rates on new residential PV systems in Italy already reach 84% — a signal of how embedded storage economics have become. The C&I segment is following.

Poland, Romania, and the broader Eastern European market offer high price volatility, rapidly expanding solar pipelines, and relatively low BESS competition. Italy, Germany, Poland, and the Czech Republic sit among the European markets with the highest C&I BESS potential due to grid congestion, energy price volatility, and regulatory support. First-mover advantage in these markets for EPCs and distributors willing to build local knowledge is real.

Spain has transformed from minimal storage activity to one of the fastest-growing markets in Europe in 24 months, driven by solar penetration that now regularly produces midday price suppression. Spain had the fifth largest battery storage fleet in Europe by end of 2024, with utility-scale revival expected to drive further growth in 2025.

Italy combines high retail electricity prices, strong solar irradiance, a mature PV installation base, and progressive energy community legislation. Battery attachment rates on new residential PV systems in Italy already reach 84% — a signal of how embedded storage economics have become. The C&I segment is following.

Poland, Romania, and the broader Eastern European market offer high price volatility, rapidly expanding solar pipelines, and relatively low BESS competition. Italy, Germany, Poland, and the Czech Republic sit among the European markets with the highest C&I BESS potential due to grid congestion, energy price volatility, and regulatory support. First-mover advantage in these markets for EPCs and distributors willing to build local knowledge is real.

A Reference Point: Commercial Battery Storage in Operation

ZTTEK's Sentinal 261 — a 261 kWh liquid-cooled C&I BESS cabinet — is currently operating on a 450 kW solar farm in Wallhausen, Germany. It's our first operational C&I deployment in the European market, and it demonstrates the core use case: capture surplus PV generation, avoid negative-price export windows, discharge when prices recover.

The Sentinal cabinet series is designed specifically for this application profile — liquid-cooled for thermal stability, IP54 for outdoor deployment, RS485/CAN and cloud API for third-party EMS integration, and certified to IEC 62619, IEC 63056, CE-EMC, CE-LVD, and CEI 0-21 for EU market deployment. Cabinet configurations are available in 233 kWh / 105 kW and 261 kWh / 125 kW, with multi-cabinet parallel expansion supported.

For sites and projects where the use case fits, we're happy to talk through the configuration.

The Sentinal cabinet series is designed specifically for this application profile — liquid-cooled for thermal stability, IP54 for outdoor deployment, RS485/CAN and cloud API for third-party EMS integration, and certified to IEC 62619, IEC 63056, CE-EMC, CE-LVD, and CEI 0-21 for EU market deployment. Cabinet configurations are available in 233 kWh / 105 kW and 261 kWh / 125 kW, with multi-cabinet parallel expansion supported.

For sites and projects where the use case fits, we're happy to talk through the configuration.

What to Do Next

If you're an EPC or system integrator evaluating C&I BESS options for European projects, the most useful next step is usually a project-specific conversation — site load profile, PV size, grid connection, target use cases, and expected tariff structure all affect system design and business case significantly.

If you're a C&I energy buyer trying to understand whether storage makes sense for your facility, the same applies. The generic payback estimates you'll find in market reports are directionally useful. The number that matters is the one calculated for your site.

We're building our European project reference base and actively looking for the right early partners in Spain, Italy, Poland, and other emerging markets. If you're working on something worth exploring, we'd like to hear about it.

If you're a C&I energy buyer trying to understand whether storage makes sense for your facility, the same applies. The generic payback estimates you'll find in market reports are directionally useful. The number that matters is the one calculated for your site.

We're building our European project reference base and actively looking for the right early partners in Spain, Italy, Poland, and other emerging markets. If you're working on something worth exploring, we'd like to hear about it.